What Medicare Still Does Not Cover in 2026 — And Why Seniors Need a Backup Plan

Medicare is one of the most important programs in America. For millions of seniors, it is the difference between getting care and going without care. But here is the part many people do not learn until they are already sitting at the doctor’s office, dentist’s office, pharmacy counter, or hospital billing desk:

Medicare does not cover everything.

That surprises people. They worked. They paid taxes. They reached Medicare age. They enrolled. Then one day they discover that certain bills are still their responsibility.

And nobody enjoys that kind of surprise. It is the healthcare version of opening the refrigerator at midnight and finding out someone finished the cheesecake.

The truth is simple: Medicare is strong, but it has gaps. Some gaps are small. Some are expensive. Some can be planned for. Others catch people off guard because they assumed Medicare worked like full lifetime medical protection.

It does not.

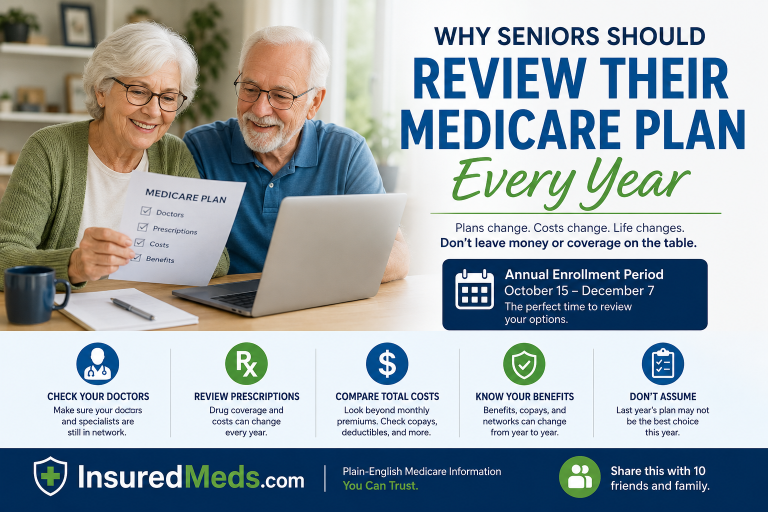

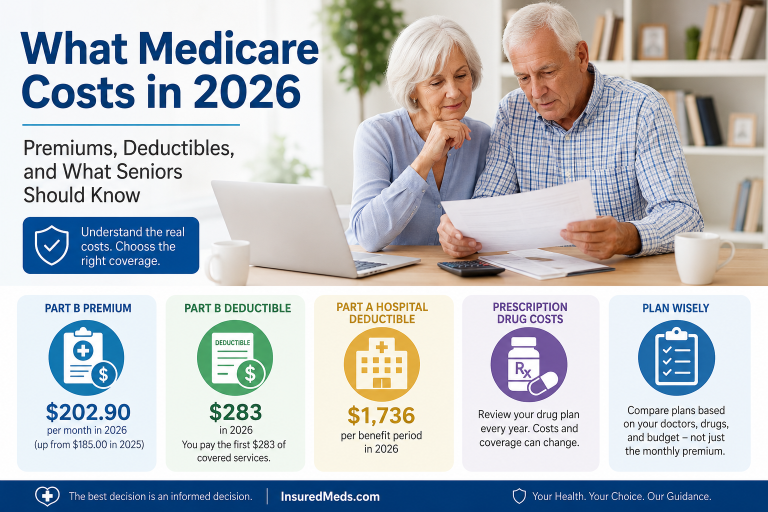

In 2026, understanding what Medicare does and does not cover is more important than ever. Medicare costs have increased, and seniors need to know where the risks are before the bill arrives. The standard Medicare Part B premium is $202.90 per month in 2026, and the annual Part B deductible is $283.

That is before we even talk about dental work, eyeglasses, hearing aids, long-term care, prescription costs, copays, coinsurance, and uncovered services.

So let’s walk through this clearly.

No scare tactics. No sales pressure. Just the facts seniors and families need to know.

Medicare Is Not One Big Blanket

Many people talk about Medicare as if it is one single plan. It is not.

Medicare has different parts:

Part A generally helps with hospital care.

Part B helps with doctor visits, outpatient care, preventive services, durable medical equipment, and many medically necessary services.

Part D helps with prescription drug coverage.

Medicare Advantage plans are private plans that replace Original Medicare as the way you receive your Medicare benefits. These plans may include extra benefits, but those benefits vary by plan, county, network, and year.

That last part is important.

A benefit you have this year may not be the same next year. A plan that includes dental, vision, hearing, transportation, or fitness benefits today may change those extras in the future. Recent reporting has already warned that some Medicare Advantage plans may reduce extra benefits in 2027 if financial pressure continues.

That does not mean every plan will cut benefits. It does mean seniors should not assume that “extra benefits” are permanent.

That is why reviewing coverage every year matters.

What Original Medicare Does Not Usually Cover

Medicare.gov clearly lists several services that Original Medicare generally does not cover. These include routine eye exams for prescription glasses, long-term care, cosmetic surgery, massage therapy, routine physical exams, hearing aids, and exams for fitting hearing aids.

Let’s break that down in plain English.

1. Routine Dental Care

This is one of the biggest surprises.

Original Medicare generally does not cover routine dental care such as cleanings, fillings, dentures, extractions, and routine dental exams.

That matters because dental problems are not just about teeth. Poor oral health can affect eating, nutrition, confidence, infection risk, and overall quality of life.

For seniors, dental care can become expensive quickly. A crown, bridge, dentures, implants, or multiple extractions can turn into a bill that feels like it needs its own mortgage.

Some Medicare Advantage plans may offer dental benefits, but the details matter. A plan may say it includes dental, but that does not automatically mean it covers every dental procedure fully.

Always check:

What is the annual dental allowance?

Are there network restrictions?

Are dentures covered?

Are implants covered?

Are root canals covered?

Is there a waiting period?

Does the plan cover preventive dental only, or major dental too?

The word “dental” on a benefits sheet is not enough. You need the fine print.

2. Routine Vision Care

Original Medicare generally does not cover routine eye exams for prescription eyeglasses or contact lenses. Medicare.gov lists eye exams for prescription eyeglasses among services Medicare does not cover.

Now, Medicare may cover some medically necessary eye care. For example, care related to diabetes, glaucoma testing for certain high-risk people, cataract surgery, and certain eye diseases may be covered under specific rules.

But routine vision is different.

That means many seniors still pay out of pocket for:

Eye exams

Prescription glasses

Bifocals

Progressive lenses

Contact lenses

Lens upgrades

Frames

And let’s be honest, eyeglasses are not cheap anymore. You walk in for a simple pair of glasses and somehow end up feeling like you just priced a used car.

Some Medicare Advantage plans may include vision benefits, but again, the limits matter. A plan might offer an allowance, but it may not cover the full cost of premium lenses or designer frames.

3. Hearing Aids

This is another big one.

Original Medicare generally does not cover hearing aids or exams for fitting hearing aids. Medicare.gov specifically lists hearing aids and exams for fitting them as services Medicare does not cover.

That can be a serious problem.

Hearing loss is not just an inconvenience. It can affect communication, confidence, social life, safety, and even emotional well-being. When people cannot hear clearly, they may withdraw from conversations. They may stop attending gatherings. They may feel embarrassed asking people to repeat themselves.

And hearing aids can be expensive.

Some Medicare Advantage plans offer hearing benefits, but they often include specific vendors, allowances, copays, or limits on device types.

Before choosing a plan because it says “hearing benefits,” seniors should ask:

What hearing aid brands are included?

Is there an allowance or a copay?

How often can hearing aids be replaced?

Are fittings included?

Are follow-up adjustments included?

Is the provider local?

A hearing benefit that looks good on paper may not be enough if the devices are limited or the provider network is inconvenient.

4. Long-Term Care

This may be the most financially dangerous misunderstanding.

Medicare generally does not cover long-term custodial care. Medicare.gov lists long-term care among services Medicare does not cover.

This is where families can get blindsided.

Medicare may cover certain skilled nursing care for a limited time if specific conditions are met. But that is not the same thing as paying for long-term help with daily living.

Long-term care can include help with:

Bathing

Dressing

Eating

Using the bathroom

Moving around safely

Supervision for memory issues

Ongoing nursing home care

Assisted living support

In-home custodial care

This kind of care can become extremely expensive.

Many families assume Medicare will step in when an older adult can no longer live independently. In many cases, that assumption is wrong.

This is why long-term care planning matters. It may involve savings, family discussions, Medicaid planning, long-term care insurance, hybrid insurance products, home safety modifications, or community-based support.

Not fun. Not glamorous. But necessary.

Because “we’ll figure it out later” is not a plan. It is a hope wearing a cheap hat.

5. Routine Physical Exams

This one confuses people because Medicare does cover certain preventive visits.

Medicare covers a Welcome to Medicare preventive visit during the first 12 months after you get Part B, if your provider accepts assignment.

Medicare also covers yearly Wellness visits to help develop or update a personalized prevention plan. But Medicare.gov clearly explains that the yearly Wellness visit is not a physical exam.

That difference matters.

A Medicare Annual Wellness Visit is not the same thing as the old-fashioned head-to-toe physical many people remember.

During a Wellness Visit, the provider may review your health risks, medications, screenings, cognitive concerns, fall risk, and prevention plan. That can be very useful.

But if you ask for a full routine physical exam, certain services may not be covered the same way.

Before scheduling, ask the doctor’s office:

Is this being billed as a Medicare Annual Wellness Visit?

Is this a physical exam?

Will there be any extra charges?

Are labs included?

Are additional concerns billed separately?

A simple question before the visit can prevent a billing headache later.

6. Cosmetic Surgery

Original Medicare generally does not cover cosmetic surgery. Medicare.gov lists cosmetic surgery among services Medicare does not cover.

There are exceptions when surgery is medically necessary, such as reconstruction after an injury or certain medically required procedures. But purely cosmetic procedures are usually not covered.

That means Medicare is not paying for someone to look twenty years younger.

If it did, there would be a line around the block and every senior center would look like a Hollywood casting office.

7. Massage Therapy and Alternative Services

Medicare.gov lists massage therapy as something Medicare does not cover.

Some people use massage, wellness services, alternative therapies, or relaxation treatments to feel better. That may be helpful for some individuals, but Original Medicare generally does not pay for everything people consider “wellness.”

This is important because wellness marketing can be confusing. Just because something sounds health-related does not mean Medicare covers it.

Before receiving a service, ask:

Is this covered by Medicare?

Is this medically necessary?

Is the provider Medicare-approved?

Will I receive a bill?

Can I get the cost in writing?

That last question is powerful. Get the cost in writing whenever possible.

8. Concierge Care

Medicare.gov also lists concierge care among services Medicare does not cover. Concierge care may also be called retainer-based medicine, boutique medicine, platinum practice, or direct care.

Some doctors charge a membership fee for special access, longer appointments, direct communication, or enhanced service.

Medicare may still cover certain covered medical services from a participating provider, but the concierge membership fee itself is generally not covered.

That means seniors should understand what they are paying for.

Ask:

What does the membership fee include?

What does Medicare still cover?

Will I still owe copays or coinsurance?

Can I use this doctor without the membership?

Is the fee monthly or annual?

Concierge care may be attractive for some people, but it is not the same as Medicare-covered care.

Preventive Services Are Still Important

Now let’s be fair.

Medicare does cover many preventive services. Medicare.gov explains that preventive services can include exams, shots, lab tests, screenings, health monitoring programs, counseling, and education to help prevent disease or detect problems early.

That is good news.

Many seniors avoid preventive care because they worry about costs. But covered preventive services can help catch problems early, and early detection can make a major difference.

Examples may include certain screenings, vaccines, counseling, and wellness visits, depending on eligibility and Medicare rules.

The important point is this:

Use the preventive benefits you have.

But do not confuse preventive benefits with full coverage for everything.

Medicare is helpful. It is not magical.

Why These Gaps Matter More in 2026

Healthcare costs continue to rise. The 2026 standard Part B premium is $202.90, up from $185.00 in 2025, and the Part B deductible is $283, up from $257 in 2025.

That may not sound dramatic to everyone, but for seniors living on fixed income, every increase matters.

A few extra dollars here, a deductible there, a dental bill, a hearing aid, a new pair of glasses, and suddenly the monthly budget starts squeaking like an old screen door.

This is why planning is not optional.

Seniors need to know:

What Medicare covers

What Medicare does not cover

What their specific plan includes

What costs they may face

What providers are in network

What prescriptions are covered

What benefits may change next year

The people who get hurt most are often the ones who assume everything is handled.

Original Medicare vs. Medicare Advantage: Know the Difference

Original Medicare does not usually include routine dental, vision, or hearing benefits. Some people add separate coverage, pay out of pocket, or consider a Medicare Advantage plan that includes extra benefits.

Medicare Advantage plans may include extras like dental, vision, hearing, fitness, transportation, over-the-counter allowances, or meal benefits. But these benefits vary by plan and location.

That is the key phrase: vary by plan and location.

Do not choose a plan only because an advertisement says “dental, vision, and hearing.”

Ask what that actually means.

A $1,000 dental allowance is different from preventive dental only.

A hearing benefit with limited device choices is different from broad hearing aid support.

A vision benefit with a small allowance may not cover the glasses you actually want.

The headline is not the contract.

How Seniors Can Protect Themselves

Here is the practical part.

Review your coverage every year

Plans change. Premiums change. Drug formularies change. Provider networks change. Extra benefits change.

Do not assume last year’s plan is still the best fit.

Check your prescriptions

Prescription drug coverage can be one of the biggest sources of surprise costs. Make sure your medications are covered and check whether they require prior authorization, step therapy, or quantity limits.

Confirm your doctors

A plan is not helpful if your preferred doctors are not in network.

Before enrolling, check the network directly with the plan and the doctor’s office.

Look beyond the premium

A $0 premium plan may still have copays, coinsurance, deductibles, network rules, and out-of-pocket costs.

The premium is only one piece of the puzzle.

Ask about dental, vision, and hearing details

Do not accept vague answers.

Ask about allowances, networks, covered services, limits, and replacement schedules.

Plan for long-term care separately

Medicare is not a long-term care plan.

Families should discuss this early, before a crisis happens.

Use Medicare.gov and licensed help

Medicare.gov is the official federal source. Licensed agents can also help explain options, but seniors should avoid pressure, rushed decisions, or anyone claiming one plan is automatically best for everyone.

No plan is best for everyone.

That is sales talk, not reality.

The Bottom Line

Medicare is valuable. Medicare is necessary. Medicare helps millions of people receive care.

But Medicare is not complete protection from every healthcare cost.

In 2026, seniors need to understand the gaps clearly, especially dental, vision, hearing, long-term care, routine physical exams, and services Medicare does not consider medically necessary.

The goal is not to be afraid.

The goal is to be prepared.

Because in Elderhood, confidence does not come from pretending everything is covered.

Confidence comes from knowing what is covered, knowing what is not covered, and making smart decisions before the bill shows up.

That is how you protect your health, your money, and your peace of mind.

Read other blog:- Read Now

FAQ

Does Medicare cover dental care in 2026?

Original Medicare generally does not cover routine dental care such as cleanings, fillings, dentures, and most routine dental procedures. Some Medicare Advantage plans may offer dental benefits, but coverage varies by plan.

Does Medicare cover eyeglasses?

Original Medicare generally does not cover routine eye exams for prescription eyeglasses. Some medically necessary eye care may be covered under specific circumstances, and some Medicare Advantage plans may offer vision benefits.

Does Medicare cover hearing aids?

Original Medicare generally does not cover hearing aids or exams for fitting hearing aids. Some Medicare Advantage plans may include hearing benefits, but the details vary.

Does Medicare pay for long-term nursing home care?

Medicare generally does not cover long-term custodial care. It may cover certain skilled nursing care for a limited time if specific rules are met, but that is not the same as long-term care.

Is the Medicare Annual Wellness Visit the same as a physical?

No. Medicare.gov states that the yearly Wellness visit is not a physical exam. It is designed to help create or update a personalized prevention plan.

What is the Medicare Part B premium in 2026?

The standard Medicare Part B premium is $202.90 per month in 2026. The annual Part B deductible is $283.

Can Medicare Advantage plans cover things Original Medicare does not?

Yes, some Medicare Advantage plans may offer extra benefits such as dental, vision, hearing, fitness, transportation, or over-the-counter allowances. These benefits vary by plan, county, and year.

Should seniors review their Medicare plan every year?

Yes. Plans can change premiums, networks, drug coverage, copays, and extra benefits each year. Reviewing coverage annually can help avoid surprises.