What Medicare Costs in 2026: Premiums, Deductibles, and What Seniors Should Know

Medicare is not free.

That surprises a lot of people when they first turn 65. After paying into the system for decades, many seniors assume Medicare will simply take over and cover everything.

Unfortunately, that is not how it works.

Medicare helps tremendously, but there are still premiums, deductibles, copays, coinsurance, drug costs, and possible out-of-pocket surprises. And in 2026, several Medicare costs have gone up.

For many seniors living on Social Security, pensions, savings, or fixed income, even a small monthly increase matters. That extra $10 or $20 is not just a number. It is groceries, gas, prescriptions, or part of the electric bill.

So let’s break this down in plain English.

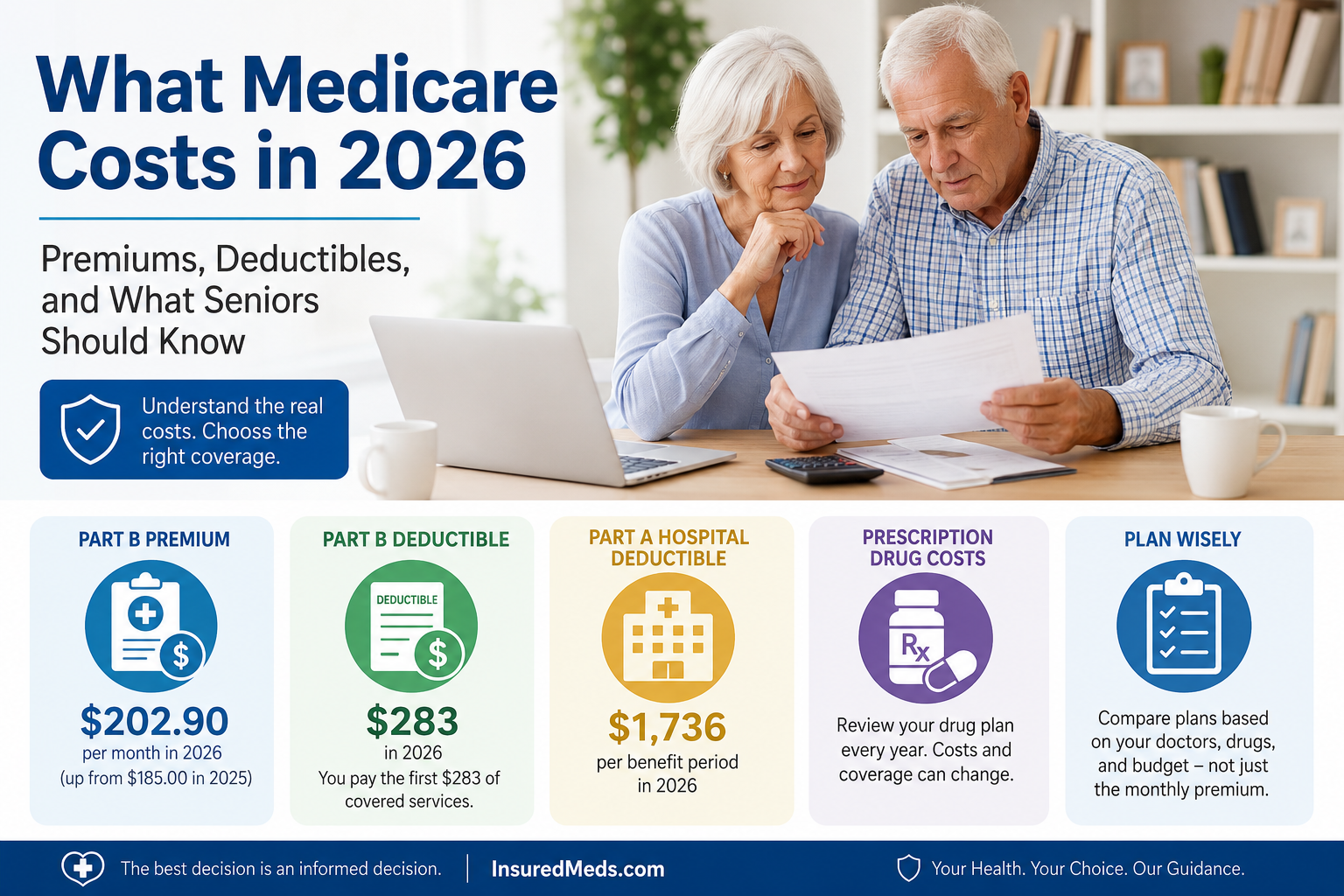

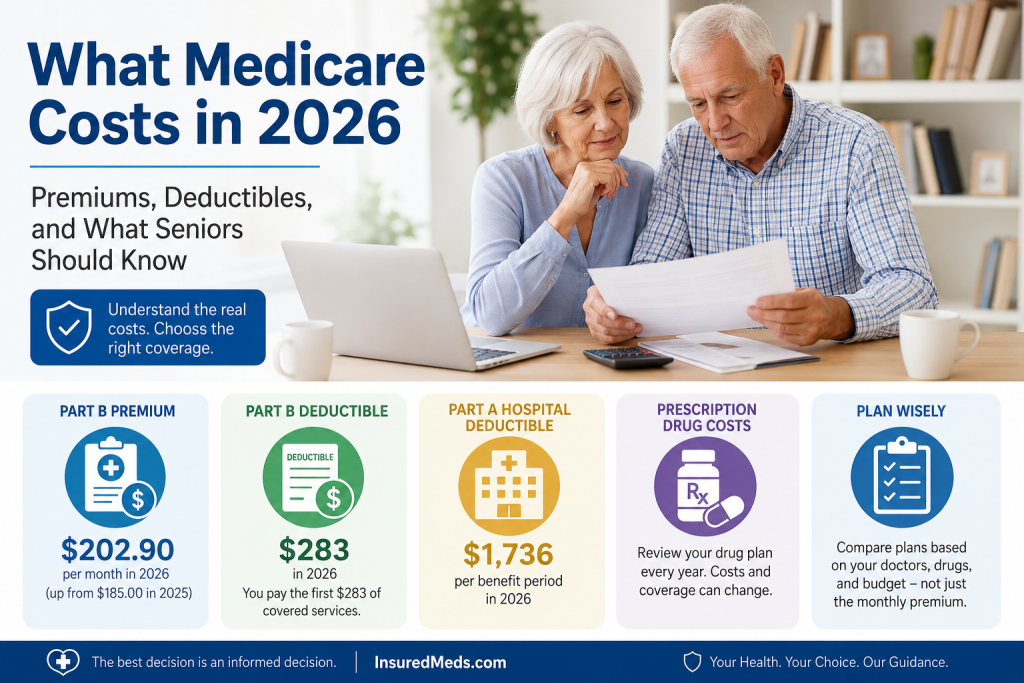

The 2026 Medicare Part B Premium

For 2026, the standard Medicare Part B monthly premium is $202.90. That is an increase from $185.00 in 2025. Medicare Part B is the part of Medicare that generally helps cover doctor visits, outpatient care, preventive services, durable medical equipment, and many medically necessary services.

Most people pay the standard Part B premium, but higher-income beneficiaries may pay more because of something called IRMAA, which stands for Income-Related Monthly Adjustment Amount.

That is government language for: “If your income is higher, your Medicare premium may be higher too.”

The 2026 Medicare Part B Deductible

The Medicare Part B deductible for 2026 is $283. That means you generally must pay the first $283 of covered Part B services before Medicare starts paying its share.

After the deductible is met, Original Medicare usually pays 80% of the Medicare-approved amount for covered services, and you are responsible for the remaining 20%, unless you have other coverage such as a Medicare Supplement plan.

That 20% can become a big deal if you have repeated doctor visits, outpatient procedures, therapy, diagnostic testing, or medical equipment.

Medicare Part A Costs in 2026

Medicare Part A is often called hospital insurance. Many people do not pay a monthly premium for Part A because they or their spouse worked and paid Medicare taxes long enough.

But “premium-free” does not mean “cost-free.”

For 2026, the Medicare Part A inpatient hospital deductible is $1,736 per benefit period. The daily coinsurance for hospital days 61 through 90 is $434 per day, and lifetime reserve days are $868 per day. Skilled nursing facility coinsurance for days 21 through 100 is $217 per day.

That is why hospital coverage can get expensive fast, especially if a person has a long stay or repeated admissions.

Why Medicare Costs Matter More Than Ever

The danger is not just one single cost. It is the combination.

A senior may have:

Part B premium

Prescription drug costs

Dental costs

Vision costs

Hearing costs

Copays

Deductibles

Transportation costs

Over-the-counter health expenses

Supplement premiums

Possible hospital or skilled nursing costs

One or two of these may be manageable. Put them all together, and Medicare planning becomes serious business.

This is why seniors should not choose a Medicare plan based only on the monthly premium. A plan with a low premium may still have copays, restrictions, networks, drug costs, or out-of-pocket limits that matter later.

Original Medicare vs. Medicare Advantage

Original Medicare includes Part A and Part B. Many people add a Part D prescription drug plan and possibly a Medicare Supplement plan.

Medicare Advantage, also called Part C, is offered by private insurance companies approved by Medicare. These plans often include hospital, medical, and drug coverage in one plan. Some may include extra benefits such as dental, vision, hearing, transportation, gym benefits, or over-the-counter allowances.

But seniors need to look carefully.

The lowest premium is not always the best plan. You need to check:

Are your doctors in the network?

Are your prescriptions covered?

What are the copays?

What is the maximum out-of-pocket limit?

Do you need referrals?

Are your hospitals included?

Will the plan still fit your needs if your health changes?

Medicare is not a guessing game. It is a decision that affects your health, your wallet, and your peace of mind.

Prescription Drug Costs in 2026

Prescription drug coverage remains one of the biggest concerns for seniors.

Even if you feel healthy today, medications can change quickly. A new diagnosis, a new prescription, or a drug moving to a different tier can affect your yearly costs.

That is why it is important to review your prescriptions every year during Medicare Open Enrollment. Do not assume last year’s drug plan is still the best plan this year.

Medicare drug plans can change premiums, deductibles, formularies, pharmacy networks, and copays from year to year.

In plain English: yesterday’s good deal can become tomorrow’s headache.

What Seniors Should Do Before Choosing a Plan

Before enrolling or switching plans, gather your information.

Make a list of:

Your doctors

Your specialists

Your hospitals

Your prescriptions

Your preferred pharmacy

Your monthly budget

Your travel habits

Any dental, vision, or hearing needs

Then compare plans based on your real life, not just the advertisement.

A television commercial does not know your doctor. A postcard does not know your prescriptions. A telemarketer does not know your health history.

That is why careful comparison matters.

Beware of Medicare Confusion

Many seniors are bombarded with Medicare mail, phone calls, television ads, and online promotions.

Some of it is useful. Some of it is confusing. Some of it is designed to rush people into action.

The best rule is simple: slow down.

You do not have to make a Medicare decision because someone calls you. You do not have to respond to every postcard. You do not have to believe every promise about “free” benefits.

Free is a dangerous word when it comes to Medicare. Something may have a $0 premium, but that does not mean there are no costs, rules, limits, or tradeoffs.

The Bottom Line

Medicare is valuable, but it is not automatic financial protection.

In 2026, seniors need to understand the real costs of Medicare before choosing a plan. That means looking beyond the premium and checking deductibles, copays, prescription coverage, networks, and out-of-pocket risks.

The goal is not just to enroll.

The goal is to enroll wisely.

At InsuredMeds.com, our mission is to help seniors understand Medicare in plain English, without pressure, confusion, or sales tricks.

Because when it comes to Medicare, the best decision is an informed decision.

FAQ: Medicare Costs in 2026

What is the Medicare Part B premium in 2026?

The standard Medicare Part B premium in 2026 is $202.90 per month. Some people with higher income may pay more.

What is the Medicare Part B deductible in 2026?

The Medicare Part B deductible in 2026 is $283. After meeting the deductible, most people with Original Medicare generally pay 20% of the Medicare-approved amount for covered Part B services.

Is Medicare Part A free?

Many people pay no monthly premium for Medicare Part A because they or their spouse worked and paid Medicare taxes long enough. However, Part A still has deductibles and coinsurance for hospital and skilled nursing facility care.

What is the Medicare Part A hospital deductible in 2026?

The Medicare Part A inpatient hospital deductible in 2026 is $1,736 per benefit period.

Does Medicare cover all medical bills?

No. Original Medicare does not cover everything. Seniors may still have deductibles, coinsurance, prescription drug costs, dental costs, vision costs, hearing costs, and other out-of-pocket expenses.

Should I choose a Medicare plan based only on the monthly premium?

No. A low monthly premium can look attractive, but seniors should also check doctor networks, prescription coverage, copays, deductibles, hospital access, and maximum out-of-pocket costs.

Can Medicare Advantage plans change every year?

Yes. Medicare Advantage plans can change benefits, networks, drug coverage, copays, and other details each year. That is why seniors should review their coverage annually.

When should seniors review their Medicare coverage?

Most people should review their Medicare coverage during the Annual Enrollment Period, which runs from October 15 through December 7 each year.

Read other blog:- Read Now