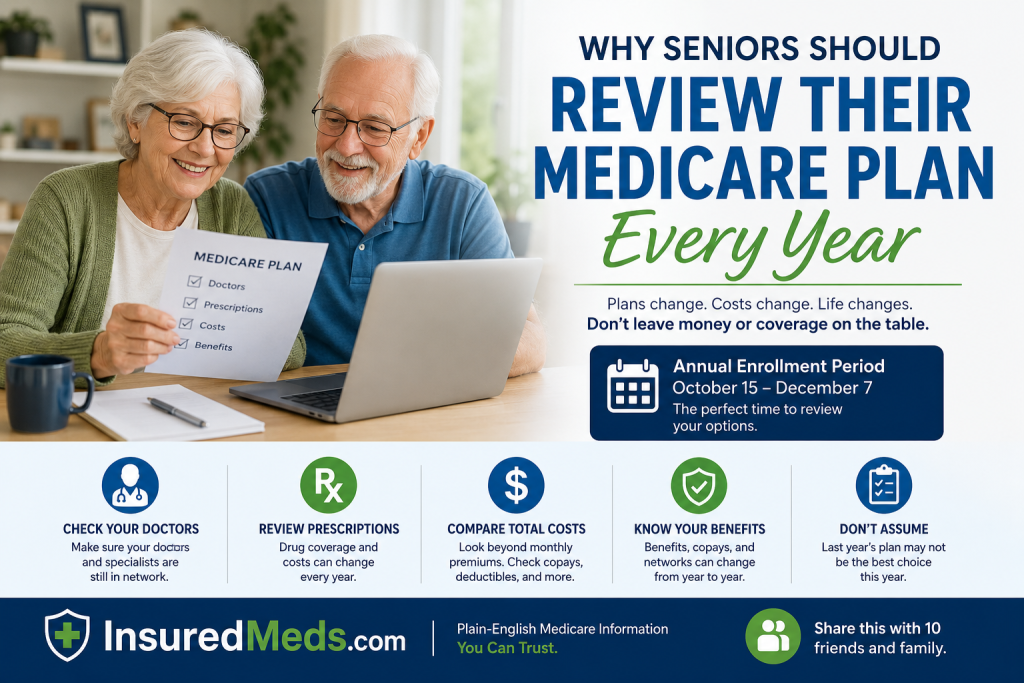

Why Seniors Should Review Their Medicare Plan Every Year

Most seniors do not want to spend their free time reading Medicare documents.

That is understandable.

Medicare paperwork is not exactly beach reading. Nobody says, “I can’t wait to curl up tonight with my Evidence of Coverage booklet.” That would worry the family.

But here is the plain truth: reviewing your Medicare plan every year can save you money, prevent surprises, and help protect your access to doctors, hospitals, and prescription drugs.

Medicare is not a one-time decision. It changes every year. Your plan may change. Your medications may change. Your doctors may change. Your health may change. And when all those moving parts change at the same time, confusion can get expensive.

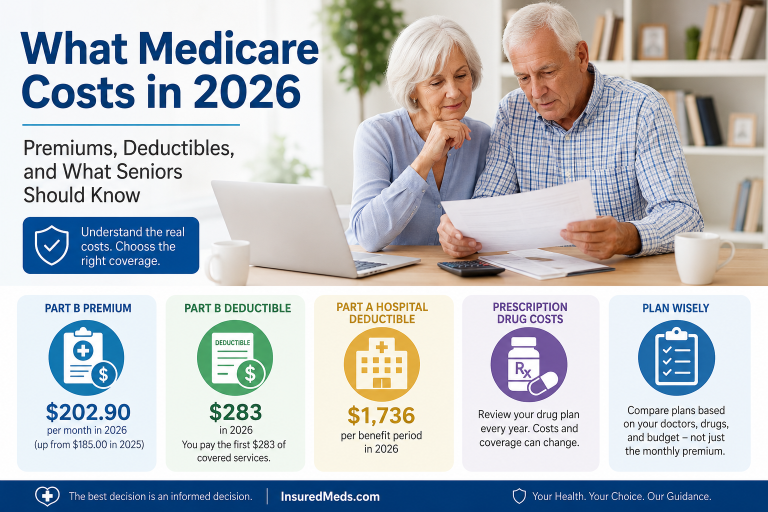

For 2026, Medicare beneficiaries should be especially careful. CMS finalized policy updates for Medicare Advantage and Part D plans for contract year 2026, including changes affecting plan accountability, prescription drug coverage, and access protections.

That means seniors should not simply assume that last year’s plan is still the best plan this year.

Sometimes it is.

Sometimes it is not.

The only way to know is to check.

Your Medicare Plan Can Change Even If You Do Nothing

One of the biggest mistakes seniors make is assuming that no action means no change.

Unfortunately, Medicare does not work that way.

If you do nothing during the Annual Enrollment Period, you may stay in your current plan automatically. But your current plan may not stay exactly the same.

A Medicare Advantage or Part D plan may change its:

Monthly premium

Doctor network

Hospital network

Drug formulary

Copays

Deductibles

Pharmacy pricing

Prior authorization rules

Extra benefits

Maximum out-of-pocket limit

That is a lot of things to change while you are just trying to enjoy your coffee.

Every fall, plans send an Annual Notice of Change. Many people ignore it because it looks like just another thick insurance mailing. But that notice tells you what is changing for the next year.

Do not throw it away too quickly.

That booklet may be boring, but boring can save money.

Your Doctor May Not Be In Network Next Year

For many seniors, the most important question is simple:

Can I keep my doctor?

This is especially important with Medicare Advantage plans because they often use provider networks.

Your primary doctor may be in network this year but not next year. A specialist may stop accepting the plan. A hospital system may change its contract. A plan may still exist, but the doctors you depend on may no longer be part of it.

That is not a small detail.

If you have a cardiologist, oncologist, neurologist, orthopedic doctor, or other specialist you trust, you should confirm they are still in network before staying with or choosing a plan.

Do not rely only on memory. Do not rely only on what your neighbor says. And do not assume that because a doctor accepted your plan last year, they will accept it next year.

Call the doctor’s office. Check the plan directory. Then double-check.

With Medicare, one check is useful. Two checks are better. Three checks are not paranoia; that is just being a senior with experience.

Prescription Drug Coverage Can Change Every Year

Prescription drug coverage is another major reason seniors should review their Medicare plan annually.

A medication that was covered this year may cost more next year. It may move to a different tier. It may require prior authorization. It may require step therapy. Or it may no longer be covered by the plan’s formulary.

CMS has continued issuing guidance on Medicare Part D benefit changes for 2026, including Part D redesign program instructions.

That matters because drug costs can vary widely from one plan to another.

Two seniors can live on the same street, have the same Medicare card, and choose the same type of coverage — but if one takes expensive brand-name medications and the other takes low-cost generics, their best plan choices may be completely different.

Before choosing a plan, make a current medication list.

Include:

Medication name

Dosage

How often you take it

Preferred pharmacy

Whether you use mail order

Any brand-name drugs

Any insulin or specialty medications

Then compare plans based on the drugs you actually take.

Not the drugs you used to take.

Not the drugs your cousin takes.

Your drugs.

Medicare is personal. Your plan should be too.

The Cheapest Premium May Not Be the Cheapest Plan

A $0 premium Medicare Advantage plan can look attractive.

And in some cases, it may be a good fit.

But a low premium does not automatically mean a low total cost.

You also need to look at copays, deductibles, coinsurance, prescription costs, out-of-pocket maximums, and network restrictions.

The cheapest plan on paper may become expensive when you actually use healthcare.

That is the trap.

It is like buying cheap shoes and then spending six months complaining about your feet. The price looked good. The experience did not.

When reviewing Medicare coverage, ask:

What is the monthly premium?

What are the doctor copays?

What are the specialist copays?

What will my medications cost?

What is the hospital cost?

What is the maximum out-of-pocket limit?

Are my doctors in network?

Are my pharmacies preferred?

Are extra benefits actually useful to me?

Do not choose a Medicare plan by premium alone.

Choose it by total value.

Extra Benefits Are Nice — But Medical Coverage Comes First

Many Medicare Advantage plans advertise extra benefits such as dental, vision, hearing, transportation, fitness memberships, over-the-counter allowances, and other perks.

Those benefits can be useful.

But they should not distract you from the core issue: medical coverage.

A dental benefit is nice. A gym benefit is nice. An over-the-counter allowance is nice.

But if your doctor is out of network, your medication is expensive, or your specialist requires prior authorization, those extras may not feel so wonderful.

Do not choose a plan because of the shiny add-ons.

Choose a plan because it protects your health, your doctors, your prescriptions, and your budget.

The extras are dessert.

Medical coverage is the meal.

And at our age, we know better than to eat only dessert — even if cheesecake makes a strong argument.

Star Ratings Can Help, But They Are Not the Whole Story

Medicare uses Star Ratings to help beneficiaries compare Medicare Advantage and Part D plans. These ratings are meant to give quality and performance information to help people choose coverage during open enrollment. CMS publishes technical information explaining how the Part C and Part D Star Ratings are created.

Star Ratings can be useful, but they should not be your only decision tool.

A highly rated plan may still not include your doctor.

A lower-rated plan may cover your medication better.

A plan with good customer service scores may still have a hospital network that does not work for you.

Use Star Ratings as one piece of the puzzle, not the whole puzzle.

The best Medicare plan is not always the plan with the best advertising or the highest rating.

The best plan is the one that fits your real life.

What About Original Medicare and Medigap?

If you have Original Medicare with a Medicare Supplement plan, also called Medigap, your yearly review may look different.

Medigap plans are standardized by letter in most states, but premiums can still change. Your Part D prescription drug plan can also change every year.

So even if you are comfortable with your Medigap coverage, you should still review your Part D drug plan annually.

Many people with Original Medicare and Medigap forget about Part D because the medical side feels stable.

That can be an expensive mistake.

Drug plans are where many surprises happen.

Review your prescription coverage every year, even if you love your Medicare Supplement plan.

When Should Seniors Review Their Medicare Plan?

The main time to review Medicare coverage is during the Medicare Annual Enrollment Period.

This period usually runs from October 15 to December 7 each year. During this time, beneficiaries can review options and make certain changes for the following year.

This is when many people compare Medicare Advantage plans and Part D prescription drug plans.

But you do not have to wait until the last minute.

In fact, waiting until the last few days is how people end up making rushed decisions.

Start early. Gather your medication list. Confirm doctors. Review your Annual Notice of Change. Compare total yearly costs.

Medicare decisions are easier when you are not racing the calendar.

And let’s be honest — rushing rarely improves anything after 65, except maybe getting to the bathroom.

What Seniors Should Check Before Staying With the Same Plan

Before you allow your Medicare plan to renew, check these items:

Are my doctors still in network?

Are my specialists still in network?

Are my hospitals still covered?

Are my prescriptions still on the formulary?

Did my drug tiers change?

Did my pharmacy pricing change?

Did my premium change?

Did my copays change?

Did my maximum out-of-pocket limit change?

Are prior authorization rules different?

Do the extra benefits still help me?

This review does not have to be complicated.

But it does need to be done.

Think of it like checking the oil in your car. You do not need to be a mechanic. But ignoring it can get expensive.

Do Not Let Pressure Decide for You

Medicare marketing can be aggressive.

Seniors may get phone calls, mailers, TV ads, Facebook ads, and conversations with people who make everything sound urgent.

Be careful.

A good Medicare decision should not feel like someone is pushing you into a chair and saying, “Sign here before your coffee gets cold.”

You are allowed to slow down.

You are allowed to ask questions.

You are allowed to compare.

You are allowed to say, “I need to review this first.”

That is not being difficult.

That is being smart.

Final Thought

Reviewing your Medicare plan every year is not just paperwork.

It is protection.

It protects your doctors. It protects your prescriptions. It protects your budget. It protects your peace of mind.

The plan that worked last year may still be right for you. But you should not assume it.

Medicare changes. Plans change. Life changes.

So every year, take a little time to check.

A few minutes of review can prevent a year of regret.

And when it comes to Medicare, that is time well spent.

FAQ

Why should I review my Medicare plan every year?

You should review your Medicare plan every year because premiums, copays, drug coverage, doctor networks, pharmacy pricing, and benefits can change. Your health and medications may also change.

Can my Medicare Advantage plan change even if I stay enrolled?

Yes. Medicare Advantage plans can change costs, provider networks, hospital networks, benefits, and rules each year. That is why you should read your Annual Notice of Change.

Can my prescription drug plan change every year?

Yes. Medicare Part D plans can change formularies, drug tiers, pharmacy networks, deductibles, and copays. Always check your current prescriptions before staying with the same drug plan.

Is a $0 premium Medicare Advantage plan really free?

No. A $0 plan premium does not mean you have no costs. You may still pay your Part B premium, copays, coinsurance, deductibles, and prescription drug costs.

Should I choose the Medicare plan with the highest Star Rating?

Not automatically. Star Ratings can help, but you should also check your doctors, hospitals, medications, pharmacies, and total costs.

Do I need to review my plan if I have Medigap?

Yes. Even if your Medigap coverage is stable, your Part D prescription drug plan can change every year. You should review your drug coverage annually.

When is the Medicare Annual Enrollment Period?

The Medicare Annual Enrollment Period usually runs from October 15 to December 7 each year. During this period, many beneficiaries can review and change Medicare Advantage or Part D plans.

What is the most important thing to check before keeping my plan?

The most important things to check are your doctors, prescriptions, pharmacies, hospitals, total yearly costs, and out-of-pocket limits.

Is InsuredMeds.com affiliated with Medicare?

No. InsuredMeds.com is an independent educational insurance resource and is not affiliated with the federal Medicare program. This article is for educational purposes only and should not be considered financial, medical, or legal advice.

Read other blog:- Read Now